For a developing country, debt accumulation is inevitable for national governments. Government spending is typically financed by government borrowing – externally and domestically – and by raising taxes. However, it is equally vital to have a sustainable debt management framework so as to avoid over-borrowing. National and sub-national governments must incorporate some kind of inter-temporal framework in their borrowing strategy such that consumption today does not mean liability for tomorrow’s generation.

In Nigeria, the Debt Management Office is the institution saddled with the responsibility of managing the nation’s sovereign debts. Periodically, it conducts stress tests to ascertain the sustainability of the debt stock against the prevailing macroeconomic environment and the scenarios in the domestic (debt) market.

The last Debt Sustainability Analysis conducted in 2017 by the DMO adopted the latest version of the joint World Bank/IMF Debt Sustainability Framework for Low-Income Countries which provides indicative debt thresholds that reflect the quality of a country’s policies and institutions. It is based on the World Bank/IMF’s Country Policy and Institutional Assessment (CPIA) index ranking which classifies countries into one of the three policy performance categories: Weak Policy (CPIA<3.25); Medium Policy (3.25≤CPIA≤3.75) and Strong Policy (CPIA >3.75), and applies different indicative debt thresholds, depending on the performance category. Along with such countries as Ghana, Mozambique, Ethiopia and Sierra Leone, Nigeria is classified as a medium performer on the CPIA index with a score of 3.41.

The 2017 DSA included a stress test for the economy under three scenarios: the baseline scenario which hinges on assumptions of the annual budget and the medium-term expenditure framework (MTEF) 2018-2020; the optimistic scenario anchors on the optimism of the Economic Recovery and Growth Plan (ERGP) with a target growth rate of 4.80% in 2018 and 7% by 2020; while the pessimistic scenario assumes continued shock to the foreign exchange earner – crude oil – at less than $30pbd, deterioration in the external balance and depreciation of the domestic currency.

Total Public debt stock (H1 2019)

| National debt | 2018 | 2019 | Diffrence | %change |

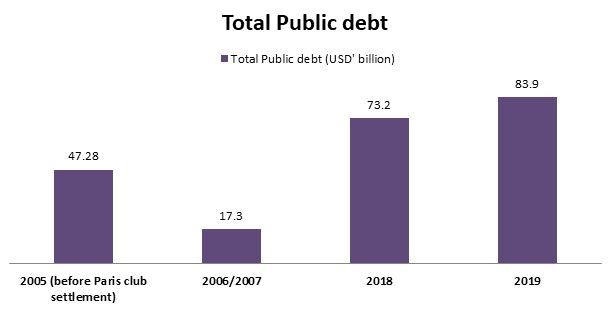

| Total Public debt (USD ‘bn) | 73.2 | 83.9 | *10.7 | 14.62 |

| External Debt (USD ‘bn) | 22.08 | 27.16 | 5.08 | 23.01 |

| Domestic Debt (NGN ‘trn) | 12.15 | 17.38 | 5.23 | 43.01 |

| Domestic Debt (USD ‘bn)* | 51.12 | 57.74 | 5.62 | 10.99 |

However, since the GDP growth rate has hovered below 2 per cent behind the ERGP optimism of 4.80%, but global oil price has hovered around USD60pb, and the naira exchange rates have been stable at N359/USD1; it may be objective to evaluate based on the baseline scenario since the scenarios in the other extremes have not been experienced.

As of June 30 2019, the Debt Management Office (DMO) reported that the debt stock (both national and sub-national) stood at N25.7 trillion (USD83.9 billion)—this represents a 14.6 per cent increase from the preceding year. Of this total, domestic debt accounts for 67.6 per cent (= N17.38 trillion), while external debt standing at N8.32 trillion (USD27.16 billion) accounted for 32.38 per cent.

In 2018, the Debt Management Office (DMO) proposed an extension of the borrowing threshold from 19.39 per cent to 25 per cent. However, with the addition of N10.7 trillion in 2019, Nigeria already surpassed the 25 per cent threshold (see Table 1). Figure 1 shows that since-after the Paris club debt write off, the nation’s public debt stock has risen by over USD65 billion – more than twice the debt written off. The DMO also adopted a strategy to increase the ratio of domestic to foreign debt as a cushion to external (foreign currency) shocks. Table 1 shows, however, that the rate of change of domestic debt is lower (11 per cent) in terms of the foreign currency than in domestic currency (N43.1 per cent). This would be due to the exchange rate effect. Should the DMO revise or revisit its debt strategy?

Sinking Funds

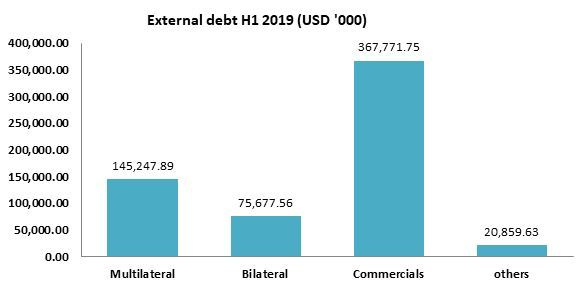

In the first half of 2019, the total amount of external debt servicing and interest payment on domestic instruments amounted USD 609.56 million and NGN800.11 billion respectively. These values are 2.2 per cent and 4.6 per cent of their corresponding total. Commercial papers and Eurobonds took 62.2 per cent of the total debt service funds while bilateral debts got the least – 3.4 per cent in Q2 2019.

For domestic debts servicing, FGN bonds claimed more than half of the total interest repayment in the first half of 2019; whereas FGN savings bond had the least with NGN658.54 million. From the table, most of the repayments were done in the first quarter of 2019 valued at NGN610.3 billion – representing 76.3 per cent of the total. And the FGN bond took NGN 480.85 billion.

Table 3 External Debt H1 2019 (USD’ 000)

| External Debt H1 2019 | |||||

| Debt servicing | Q1 2019 | Q2 2019 | Q1 % of total | Q2 % of total | H1 2019 |

| Multilateral | 79,397.93 | 65,849.96 | 22.23% | 26.10% | 145,247.89 |

| Bilateral | 67,099.39 | 8,578.17 | 18.78% | 3.40% | 75,677.56 |

| Commercial/E-bond | 210,759.58 | 157,012.17 | 58.99% | 62.23% | 367,771.75 |

| others | 20,859.63 | 8.27% | 20,859.63 | ||

| Total | 357,256.90 | 252,299.93 | 100% | 100% | 609,556.83 |

Table 4 Domestic Debt H1 2019

| Int. on instruments | Q1 N’bn | Q2 N’bn | H1 N’bn |

| NTBs | 120.92 | 45.71 | 166.63 |

| Treasury Bonds | 6.25 | 6.25 | |

| FGN Bonds | 480.85 | 128.99 | 609.84 |

| FGN Savings Bonds (N’Mn) | 347.92 | 310.62 | 658.54 |

| FGN SUKUK | 8.17 | 7.85 | 16.02 |

| FGN Green Bond (N’Mn) | 718.53 | 718.53 | |

| Total | 610.28 | 189.83 | 800.11 |

Conclusion

The year 2019 has been an interesting time. Macroeconomic indicators are not impressive: inflation is above 11 per cent, GDP growth less than 2 per cent, unemployment is high above 25 per cent and debt and debt servicing continues to hover over the bars. Increased government presence in the debt market would crowd-out private sector investments and matters would be debilitating. Recently, the Central Bank of Nigeria restricted the purchase of its OMO bills to banking institutions and Foreign Portfolio Investors (FPI) in a bid to re-channel funds away from risk-free assets to real sector investments. This is expected to moderate yield environment and reallocated resources to growth sectors. However, monetary institutions have to be strategic going into the New Year to hedge against external shocks and other fundamental uncertainties.